Rock Products’ Annual Survey On The Opinions, Concerns And Buying Intentions Of Producers Reveals What Is On The Industry’s Collective Mind.

So who took the survey this year? More than 200 industry professionals contributed to the survey data. A typical survey respondent was an officer, executive, owner or partner. A production manager, foreman or technical superintendent was next. A further breakdown indicates a portion of the respondents identified themselves as sales executive or department head as well as other.

What types of operations are reflected by this year’s survey respondents?

Operations producing between 0 and 500,000 tpy were represented this year in the top tier. Plants producing more than 2.5 million tpy were next, followed by plants producing between 500 and 1.5 million tpy. Plants producing between 1.5 and 2.5 million tpy rounded out respondent’s production capacity.

The number of survey participants employed at companies that produce both crushed stone, and sand and gravel increased this year (51.02%), up from the previous survey. Producers of crushed stone represented 16.33% of the field, while producers of sand and gravel only made up 14.29% of the field.

Geographic location was dominated by operations in the Northeast and Southwest, followed by the Midwest and Southeast. The Plains and Northwest round out the geographic spread with additional response coming in from Canada and Mexico.

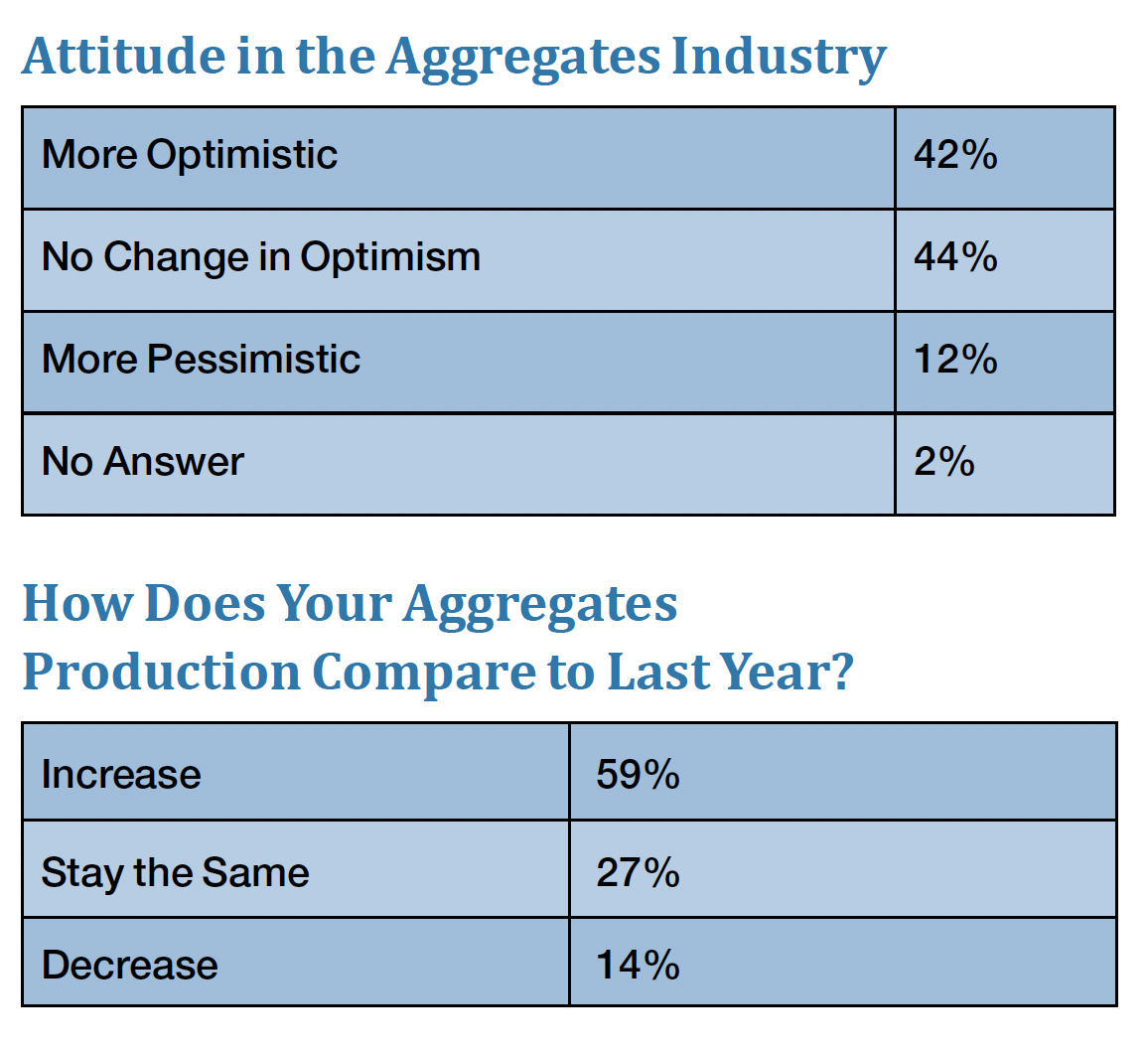

Big Issues

When it comes to the key issues facing aggregates producers, there is a new big “number-one.” While in the past, the Construction Economy and National Economy were of major concern, this year, again, it is Labor. Back again is Environmental Regulations, Permitting, State DOT logjams and Equipment Capitalization.

Equipment Capitalization

With a new federal infrastructure bill now in place, producers are starting to spend money. Just over 52% of respondents said they will increase capital spending.

A majority (35%) planned to spend $5 million to $10 million this year. About 29% planned to spend $1 million to $5 million. About 26% of the survey group planned to spend up to $500,000, while 10% planned to spend $500,000 to $1 million.

And what do they plan to buy?

- Equipment upgrades.

- New equipment.

- Plant additions.

- Technology upgrades.

- Permitting and bonding.

- Used equipment.

- Mine development.

- Safety and health changes.

- New plant construction.

- Quality control.

- Exploration.

- Reclaim systems.

- New mine start up.

Aggregates operations have specific product categories in mind when it comes to spending their upgrade dollars. They are in order:

- Replacement parts.

- Oil and lubes.

- Tires.

- Environment/Safety supplies.

- Maintenance equipment.

- Material handling/Conveying Equipment.

- Screening and sizing equipment.

- Pick-up / Utility Vehicles.

- Pumps.

- Motors.

- Excavators/loaders/dredges.

- Drilling and blasting suppliers/services.

- Crushers.

- Portable crushing/screening plants.

- Washing and classifying equipment.

- Haul trucks.

- Scales.

- Breakers.

- Automation products.

- Energy management.

- Drones.

- Frac Sand equipment.

- Other.

Impacting the Industry

Respondents were asked the question, “What will impact the U.S. aggregates industry the most in the near future and how should it prepare?” Respondents touched all the bases, some good and some bad with their responses.

- Maintaining strong pricing if inflation is tamed and input costs decrease.

- Transportation funding, inflation and federal reserve policies.

- Permitting.

- Construction economy is the biggest issue, planning for a slowdown.

- Availability of raw material to process. Permitting problems.

- Labor shortages, improved recruiting and job offers.

- Labor shortage. Increase automation.

- Economy. Permitting. Steady infrastructure funding.

- Federal budget and global warming, nobody wants to hear the solution. Labor, need more post high school age entering the work force.

- Parts availability and manpower.

- Reserve procurement and labor.

- State and federal regulations.

- Environmental regulations and the cost to comply.

- Increase in infrastructure and construction.

- Finding good labor.

- National economy, focus on flexibility in sales.

- Nationally I’d say labor issues, though that’s not been an issue for us.

- The push for electric equipment and vehicle are going to be troublesome.

- Fuel and lubricant, availability of parts and supplies, supply chain.

- Permitting, poor legislation leadership and labor.

- Federal Reserve policy and impact on economy.

- Interest rates increase – less building taking place

- I think you will see more RCA etc., due to landfill locations.

- The price of fuels used. Having to raise the price of our products and passing along to our customers

- High energy costs

- Replacing retiring employees. Increase our efforts at educating the public about the aggregate industry and the jobs that are available.

- The slowdown of the national economy, which will effect housing starts and sales.

- Labor shortages

- Concrete production.

- Recruiting and retaining team members and readily available zoned and permitted high quality reserves.

- Environmental control, personnel and water resources.

- Environmental issues only adds cost to the bottom line, how to control that is a good question. Hiring trained people in this field is very difficult nobody wants to work so that adds to more automation. The only way to control water is to store more on the property.

- Attracting employees to the industry. We can’t hire enough employees. EPA rules and regulations.

Looking Ahead

Aggregates producers are pretty confident right now that they are sitting on an acceptable amount of reserves for the foreseeable future. About 78% of respondents said they have adequate reserves, up from last survey. When asked what limits their access to reserves, respondents most cited permitting, while access to materials and NIMBY groups followed. Limited quality of materials were cited as much less of a concern this year than in past years.